What Is Money?

By Mary Logan

04 September, 2012

A Prosperous Way Down

Our obsession with money will be an issue for many as we transition from a wealth-oriented capitalist system. Many blogs focus on money—how to make more, how to keep what you’ve got, how to transition to something different and still be “ahead of the game.” Where will these voices be when the currency quits? Judging from the heavy emphasis on money in the blogosphere, many may feel dislocated when the casino chips disappear from the game. We need to look more broadly at the problem of money–those who focus on money without seeing the nature of the real system behind it are still grieving for the loss of an artifact of post industrial society. How do we deal personally with issues of debt and money in transition to economic contraction, while manipulated currencies bank on continued growth?

Our obsession with money will be an issue for many as we transition from a wealth-oriented capitalist system. Many blogs focus on money—how to make more, how to keep what you’ve got, how to transition to something different and still be “ahead of the game.” Where will these voices be when the currency quits? Judging from the heavy emphasis on money in the blogosphere, many may feel dislocated when the casino chips disappear from the game. We need to look more broadly at the problem of money–those who focus on money without seeing the nature of the real system behind it are still grieving for the loss of an artifact of post industrial society. How do we deal personally with issues of debt and money in transition to economic contraction, while manipulated currencies bank on continued growth?

My thoughts converge after a flurry of recent thoughtful articles about money, including several from permaculture.org.au. These articles converge with multiple questions from friends about the future of money. What do I do with my savings if they are becoming less valuable? Should I spend money to buy a house? Will the stock market persist as a way of gaining wealth? Should I be saving at all if money is inflating away to become less valuable?

What does money value?

All paper currencies are promises to return some value from within the system, so they are in essence IOUs that grease the wheels of trade. Odum always de-emphasized money in his writing. He was aware of its symbolism and its transitory, inaccurate meaning in a world of growth. So I frame this discussion at the meta-level, while also trying to discuss smaller individual scale concerns.

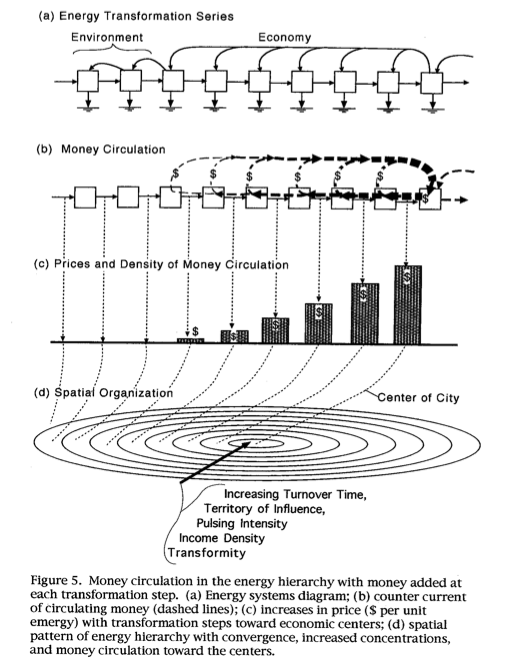

Money is a circular flow of information that flows in a circle in the opposite direction from the flow of energy and goods. Odum proposed a Hierarchy of Money as a 7th thermodynamic law.

Odum, 2000, Energy Hierarchy and Money (PDF)

“At the low levels on the left are free environmental transformations with no money. At each higher step there is value added, and thus the money concentration increases as does the energy/money ratio. The energy per unit money decreases, and vice versa, the money per unit energy (price) rises. In the centers, the circulation of money is more concentrated but the buying power of money is less. . . . In one sense energy and money are causally related. Traditional views about the creativity of human choices might regard these coupled relationships as restraints. Others might conclude that human economic behavior, including the free markets, is really not so free of system determinism and natural law” (Odum, 2000, p. 11).

While energetic systems principles may decide economic behavior, the money construct is an imperfect creation that requires faith and confidence in the representations of value that the system creates. Money measures market prices that do not include nature’s contributions. If we fail to put the economy’s work on the same basis as nature’s

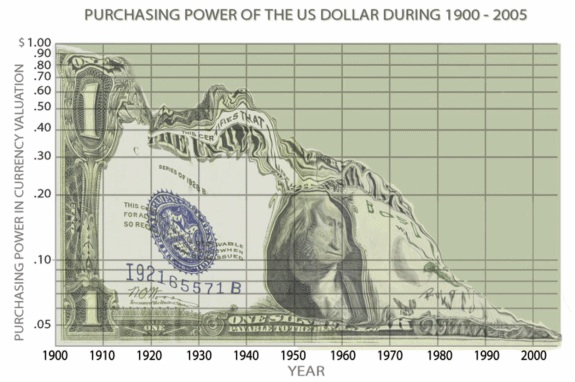

Data from BLS/Fed, original source unknown

work, we devalue and hollow out nature. What we are left with, then, in the end, is a pile of money that represents nothing, as its basis of nature has disappeared. During the Enlightenment, Voltaire said, “Don’t think money does everything or you are going to end up doing everything for money, . . . and . . . Paper money eventually returns to its intrinsic value–zero.” I guess that’s where we’re quickly headed.

“The flow of energy makes possible the circulation of money, and the manipulation of money can control the flow of energy” (Odum, 1976, p. 49). Money is a cycle which does not turn unless material cycles are turning and energy is flowing. If energy becomes less, the system must turn more slowly. Like all the other flows, money helps work processes go; but the money flow itself causes work and must thus be regarded as having its component of energy too” (p. 52). In the 1930s, stimulating the flow of money could stimulate the inflow of energy and work because there was abundant available energy. In the 1970s, rich deposits of energy-carrying materials such as petroleum, copper, and fertilizer have become scarce. The problem, then, is a shortage of available energy, and therefore money may not stimulate much more flow of energy. When the rate of inflowing energy is as high as it can be, more money cannot increase it” (Odum, 1976, p. 56).

Traditional economists equate money with resources and equate money with debt. At some point, then, debt becomes a proxy for resources, and as we expand debt, we begin to expect that pieces of paper can represent an infinite supply of available resource in the future. We have greatly expanded debt in the US over the past 3 decades as a proxy for receding energy, and as a way to better acquire external sources of energy. As our empire fails, each year we have to use more and more taxpayer money to assuage the debt. We can interpret this taxpayer payment as more and more economic labor being drained into corporate profit/wealth and non-viable economic functions. The question is whether our debt will expand faster than inflation?

If we think we can grow indefinitely, or even level off eventually in a steady state, then any debt we incur can be paid off at a later date, when things get better. If we instead believe that the economy will contract from here on out, we will have very different expectations about debt, savings, and the future.

Paul Krugman suggested recently that since debt is so cheap, we should at least make good use of it by funding education initiatives. How does that work– how do we translate printed green pieces of paper (IOUs to the future) into labor and resources in a system that is running out of gas? As energy wanes, the money circulating either remains the same or expands in the form of debt, causing inflation. Stimulating the economy with debt will no longer work. If we are to make our currency work in descent, we must instead decrease what we do, equitably, while also decreasing the money system. A system that is contracting also needs a contracting money supply. Expanding debt or printing money in the face of permanent economic contraction is a formula for inflation, hyperinflation, and currency failure. This route increases unemployment, inequality, and the potential for future strife. Yet political expediency and massive unfunded liabilities dictate that we take the easy route of printing money and not contracting the size of our economy, our government, and our obligations to the future. The good news is that inflation not only devalues savings, but it also devalues debt. Eventually we may both default and inflate, with default of debt that is held by those without power, and inflation of debt that represents promises we can’t keep but continue to hold.

So what does this mean for us as people living within the old paradigm, trying to either keep what we saved from the old dominant system, or trying to use money as capital to jump-start something in the new system? Should we incur debt? Should we save, and if so, how? Can we keep previously saved money that represents chits representing stored assets in the old economy, as financial bloggers advertise?

Austerity versus Frugality

http://online.wsj.com /article/SB120967904 813560797.html

My parents taught me the importance of frugality and savings as the means for future security and production. There is a lot of discussion in the media about the potential need for austerity at the larger economic scale, as a measure that governments impose on their people to keep what we have. Does that mean that if our governments save, then we as people don’t have to? If we take back the lost value of frugality, we have moved the locus of control to ourselves, and we have changed it into a positive virtue. On the smaller personal scale, saving assets creates a longer term storage of wealth to store assets that buffer for the future. Attempts at national austerity were abandoned in the 1980s when Reagan declared a new morning in America, creating a culture of debt. We transitioned national policies to a “spend without saving” system to keep our “non-negotiable” way of life. (Refer here to an explanation on how the petrodollar, resource imperialism, and privatization made deferral of Americans’ post-peak pain succeed.) Those pivotal habits of borrowing and spending also appeared to translate into people’s attitudes about frugality. Our ideas about personal savings have changed so radically that now, in 2012, half of Americans have no retirement savings. Essentially, reliance on debt is a form of doubling down and going for broke on the hopes that the future will always be brighter, with no alternative plan if things don’t work out. This is the sort of expectation that breeds hopelessness when dashed. It makes for desperate nations and desperate individuals.

A friend recently graduated from college is accruing money for the first time. She doesn’t have college debt–her parents saved ahead of time for her college costs. She wants to know the best way to accumulate savings. I told her that in the short-term, cash was OK. Keep a supply of cash on hand to cover emergencies. In descent, storages or savings of resources will become more important, as unstable just-in-time systems start to fail. Stability generally requires larger storages; Odum suggested two years worth as a general buffer for storages in general.

Inflationary policies also hurt those with savings, as money loses value over time. Some 30-something friends are in transition, with questions about buying land and building a very efficient small home on it. This plan would need a significant investment of time and “money.” They have money saved, which they perceive as losing value in the future, so they want to invest in something that will hold value better. They both have Masters degrees, with no immediate plans for more education. Is this the right choice for this couple in their current circumstances?

Letting their money sit in cash is a losing proposition over the long-term, since bank deposits lose value in inflation. Rescuing something from it makes sense of past labors. There are very few necessary, real assets to invest in now–a roof over your head is one of them. Owning a house is a form of forced savings, and owning your own place allows the freedom to create a resilient base and security, through vegetable gardens and other adaptations. Ownership is an investment in community, and ownership allows one to build sweat equity through improvements. Interest rates are very low now. Housing is so expensive that first time homebuyers have to start somewhere. But a lot of housing is in an expensive bubble, especially in urban areas that may contract as we descend. So buying bubbly housing or spending savings that might be needed for planned, future education, especially if people need to move soon or stay light on their feet might not be such a good idea. Decisions are not as formulaic or clear-cut as they used to be.

Debt in a contracting economy

http://www.eurozine.com/articles/2009-08-20- graeber-en.html

Investing in education or a small house to live in using savings and some debt makes sense, but not if one goes into significant, long-term debt and one cannot get adequate employment to pay back the debt. Historically, mortgages featured brief maturities of five years or less and high down payments from earlier savings. As the advantages of debt wane in a contracting economy, we may go back to those old ways. Unless debt gets inflated away or there is a debt jubilee, significant debts will default in a future without growth, especially those connected to the failing paradigm of empire. In the US, much of home mortgage debt is now held by governmental agencies. How will the meaning of bankruptcy change? Historically, debt has come and gone in local monetary systems that boomed and busted in a similar fashion. Graeber points out the central mechanism of war and slavery in creating debt. Credit systems arise during peace, while commodity-based systems are prominent during wartime. Graeber suggests that our current system is “the first effective planetary administrative system largely in order to protect the interests of creditors.” In essence, we have replaced old systems of debt slavery with fossil fuel-based slavery. History is full of examples of debt bondage. Serfdom exists in the modern world in poor countries, and it may come again to wealthy countries. While this may not happen within our generation, we are both philosophically and emotionally conscripted to the corporation, through the device of money. Voltaire said, “L’homme est libre au moment qu’il veut l’être.” We are free at the instant we want to be free.

“When limited resources cause economic leveling, interest rates may be high to prevent borrowing that can’t be repaid for lack of growth. . . Borrowing fails when neither production nor markets can expand; borrowing and high interest rates may become regarded as usury again“ (Odum, 1987). So one might argue that since interest rates are still abnormally low due to manipulation through credit swaps, that now is a good time to borrow money. But in an uncertain future, isn’t it safer to limit obligations to the empire as best one can? How much house is too much, and how do we adapt existing McMansions to a smaller way of being without enslaving ourselves to a crumbling empire?

Over the long-term, saving in typical investment securities or even holding cash is a losing proposition. Better to use it to fund education for knowledge and skills right for a downsized future. Is college or post-graduate education worth the incursion of long-term debt? Will our heavily manipulated stock and bond markets in the future of a permanently contracting economy be able to deliver returns of 5 to 10%? Reason dictates that if we do continue to get returns that high, that inflation will outpace the returns as we continue to manipulate and support the stock market casino by printing money. So I suggested to my recent graduate friend that once she had saved a stash of emergency cash, and once she had matched savings incentive plans from her job, that her money was better used in living her life to the fullest, developing skills and knowledge, following her passions, finding her aptitudes, and contributing in her unique way.

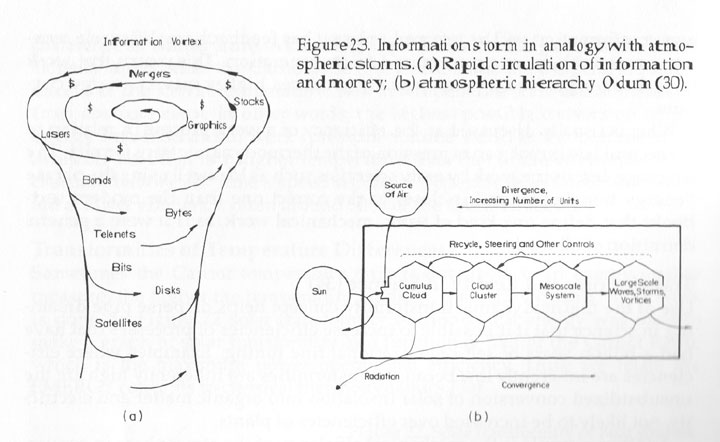

Odum, Crafoord Lecture (1987, p. 60) Information Storm

What happens when our fiat currencies die, as all currencies eventually do? It will eventually be worthless. When our monetary system fails, those who view money as a materialization or manifestation of our real economy will think that the world is ending. The end of a fiat currency is not the end of the world, particularly when money is increasingly spinning as a simulacrum in its accelerated information storm separated from real society at the upper levels of the financial system. It is only the end of the world for those emotionally invested in it as the reason for living.

After a period of dislocation, alternative modes of information exchange that grease the wheels of trade will organize. Those who view money as the end goal of our economy have underrated the importance of the real, natural world on the way up, and they will probably continue to do so on the way down, by overreacting to the demise of fiat currencies, since they are emotionally invested in money as the goal of life. When the hurricane of surreal, spinning money storm dissipates, it will leave a washed new world ready for new interpretations of money. We will only do better in solving our problem of unsustainable society if we find new ways of measuring and valuing nature.

In the meantime, we may be vulnerable to wide swings in the price of commodities that we need, such as food, education for your children, paying the monthly utilities, and preparing for a different future than empire suggests. During transition, we need to move away from the symbol of currency as a goal or a representation of self-worth. Yet many cannot divest themselves from the symbolism of currency and the status it brings. I would ask these people, are you emotionally ready to see your values fail that glorify money as the goal? How would you feel if you woke up tomorrow and your money was worthless? How would you restructure your life, and would the things that you value be different? I’m still waiting for the answers.

from Money Goes Upstream (Gary Snyder, Axe Handles, 1983, p. 101)

. . . I can smell the grass, feel the stones with bare feet

though I sit here shod and clothed

with all the people. That’s my power.

And some odd force is in the world

Not a power

That seeks to own the source.

It dazzles and it slips us by,

It swims upstream.

Mary O. Logan-UAA adjunct, Anchorage, AK, US

Comments are moderated