The BJP’s new Bankruptcy and Insolvency Rules 2016 in India bluntly provide that individuals with debts over Rupees one thousand will lose their assets to a resolution professional if declared bankrupt or insolvent. The only excluded assets under fresh start rules are tools, books, vehicles and other equipment as are necessary to the debtor or bankrupt for his personal use or for the purpose of his employment, business or vocation. But under an insolvency order even these are taken over by the resolution professional.

We cannot keep furniture, household equipment and provisions, personal ornaments, life insurance policy or pension plan, or anything not been mortgaged or otherwise given as security. We cannot exclude any liability to pay a fine imposed by a court or tribunal or to pay maintenance or a student loan. And again, under an insolvency order even assets not mortgaged or pawned are in the end taken over by the resolution professional.

The fresh start envisaged under the section 80 of part III Chapter 1 of the Rules are applicable to those of us who have an annual income of less than Rupees sixty thousand per year and assets valued less than Rupees twenty thousand and debts less than Rupees thirty-five thousand. If we own a house we cannot use the Rules. Most poor women will come under this provision as practically none of us own houses.

If we file an application for a fresh start with the local Debt Recovery Tribunal we get an interim-moratorium in relation to all the debts and no debtor is allowed to pursue us until the application is accepted or rejected. If we don’t have the support of a resolution professional, the Adjudicating Authority has to nominate one for us within seven days. And the resolution professional has to examine the application and recommend acceptance or rejection within ten days of her appointment. The resolution professional is bound to presume that the debtor is unable to pay her debts at the date of the application unless the information is false. The order passed thereafter must state the amount which has been accepted as qualifying debts by the resolution professional and other amounts eligible for discharge under section 92 for the purposes of the fresh start order. The order generally must discharge us from all liabilities except qualifying debts. Once we default on the qualifying debts for which creditors have issued us notice and we have been unable to repay, we apply for an insolvency resolution and provide all the information needed to get the relevant order. All legal action or proceedings pending in respect of any debt are deemed to have been stayed till we get the order. The resolution professional then examines the application for insolvency and gives a recommendation within ten days of his appointment. Where the resolution professional finds that the debtor is eligible for a fresh start she can change the application by the debtor under section 94 for insolvency to an application under section 81 for a fresh start. If we are found insolvent then negotiations between the debtor and creditors start for arriving at a repayment plan under section 100. Thereafter the Adjudicating Authority issues a public notice within seven days of passing the order inviting claims from all creditors within twenty-one days of such issue. The repayment plan may authorise or require the resolution professional to carry on the debtor’s business or trade on his behalf or in his name; or realise the assets of the debtor; or administer or dispose of any funds of the debtor.

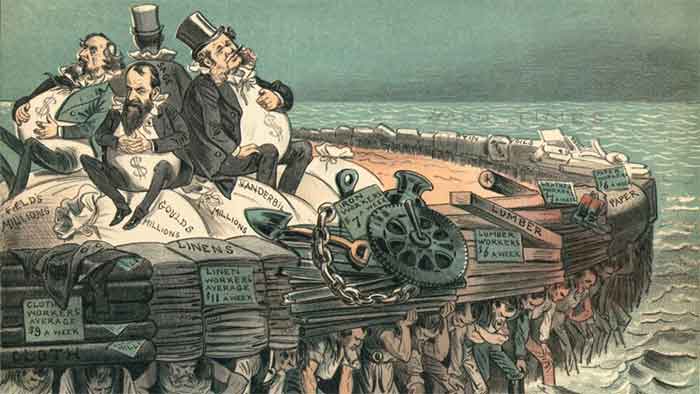

Basically these resolution professionals are like the lawyers during the British days. Everyone knows that most upper caste Indians got their land during British days by looking out for land being seized by the British for non-payment of taxes or some other reason. The lawyers and their relations then bought up that land at knock down rates and lived happily ever after. In the same way the Bankruptcy and Insolvency Rules 2016 allow resolution professionals to carry on the business or trade in the name of anyone with less than Rupees 60000 income per year and debts and assets worth less than Rupees 55’000; the resolution professional may sell off my assets to her relations, and dispose of any funds I may have as she thinks fit. I also have to pay her for this wonderful service she is providing to me. No wonder half of the 2016 Rules are devoted to dealing with replacing resolution professionals who are corrupt! The point is how can there be such a professional who is not corrupt? Inevitably the only castes and classes who can buy up my assets are those who are richer than me and who will have the wherewithal to become resolution professionals. The incredible thing is that the Rules provide that the one thing I want to avoid, which is losing my assets, is actually legally facilitated under the Rules and the transfer is done not only by but to the very person enforcing the Rules.

The Bankruptcy and Insolvency Rules for Individuals under Part III Chapter 1 of the Rules are nothing but legalised theft of the assets of the marginal poor who don’t even own a house, and are thus most likely to be the poorest of poor women; by the professional castes and classes who have the means to become resolution professionals.

The caring economy is mainly looked after by women. ‘Care’ is actually the basis of economics. It has nothing to do with supply and demand, profit and loss. It is about doing work to support humans and human relationships and the ecological regeneration on which we depend. Maharashtra, Uttar Pradesh, Punjab and Andhra Pradesh are seeking new money to monetise farm debts in their states. The Finance Minister Arun Jaitley, Narendra Modi the Prime Minister and Urjit Patel the reserve bank of India Governor are jumping up and down about the potential Rupees 250 lakh crore so called burden this will put on the Central and or State Government budgets across India as a whole. But from the point of view of the woman cultivator this is not a burden but an asset; it is our currency that we use to provide care. It is not a burden: it is our cash. But from the point of view of the Bankruptcy and Insolvency Rules 2016 we are supposed to hand over all our assets to the upper caste and class resolution professional or her relatives who have the cash to buy up our assets. Why not just give it all to the creditors to begin with like in the good old days of unregulated money-lending, and be done with it?

The only way we can get round all this is to get our own people appointed as resolution professionals so that our own families and friends can take advantage of the transfer of assets which is otherwise legalised theft of one class and caste by another under the Rules. Otherwise as usual the poor who are living most sustainably are expropriated by the state on behalf of capital for the sheer fun of it.

Anandi Sharan is an environmental historian and writer based at Bangalore. She is a Board member of the global environmental platform CBD Alliance and has been articulating the global South’s concerns on climate change. She can be reached at [email protected]