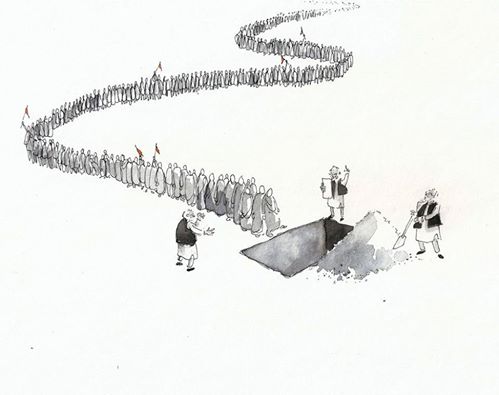

Usually, Sunday evening is peak business time for local super markets. On last Sunday, 11 December evening, many customers in super bazaars and malls had come back empty handed as credit cards were not accepted – the reason – bank servers were down and there is still Monday ahead, which happens to be a bank holiday. On Sunday morning many dailies had reported that bank servers are down on Saturday itself. This is what awaits us in the coming days. There is a rule in engineering design, which says, “when things fail, they are most likely to fail at the critical moment.’ Engineers know this only too well and try to improve reliability by improving the factor of safety and also by incorporating redundancy where ever possible. But even these measures cannot prevent a system from crashing. So you have to have spares and consumables ready on hand to handle emergencies. This is a classic case of contradiction between techies and bean counters – techies want spares and consumables along with the new equipment being installed and bean counters say that they come under current account and cannot be clubbed with capital expenditure. So many new systems are put in place without necessary spares. When overloaded, the system crashes and there is chaos everywhere. With our ramshackle infrastructure and poor quality maintenance, coupled with our “chalta hai, chal ne do” attitude of decision makers, our systems, including our much abused bank computer servers are really not equipped to handle overload. Economists and financial experts, advising those sitting atop the power pyramid, take the existing infrastructure for granted and go on preaching gospels that the country has to go ‘cashless’ – the sooner the better. But with most of those already holding cards coming to use them, the system gets overloaded and crashes. What if card usage and on-line transactions increase by, say, a factor of 10? – God forbid! – there is bound to be pandemonium everywhere. The whole country’s economy can come to a grinding halt! To install higher capacity systems and migrate to them can take months. Just recalibrating the ATMs is taking such a long time that, people curse the government whenever they come across an ATM. Which means that, with poor infrastructure in power, communications and other critical areas of the economy, any call for major and instant change will only invite a disaster. And disaster is already staring at us in the face.

Much has already been written about how 80% of Indians are not fit as per the existing bank rules to own credit and debit cards. This requires fresh breeze of changes in the way our banking system functions and such a fundamental change cannot be instantaneous. And over and above that facilitating the use of on-line facilities by uneducated and semi-educated people calls for much more innovative ways of conducting on-line bank transactions. Right now, only the educated and tech-savvy youth feel comfortable with apps on smart phones. Many highly educated elderly people feel lost when confronted with an on-line transaction – what to say of the common poor and lower middle class citizens. Crores of rural and urban poor in our country do not a have a permanent address – many of them migrate to distant pastures looking for work, as agriculture is not able to feed them. They rest their legs in ramshackle slums and try to save on the daily or weekly wages to meet expenses at home. They necessarily get paid in cash. As things stand, none of them are eligible to qualify as ‘esteemed’ bank customers. Expecting a billion people to suddenly changeover to digital currency is nothing short of pure madness, bordering on insanity. This move by the “most exalted one” is definitely going to plunge the country in to a bottomless pit of economic downward spiral.

By now, it has become amply evident that the real motive behind the demonetization is neither of the two stated goals – black money is still thriving and “God is in heaven and all is well with the world” for the black barons. The only difference now is that, black has taken the colour of purple. Neither is there much to talk home about the much hyped war on “fake” currency – a mountain has been dug to catch the proverbial rat. That the hurry to convert the nation to plastic is driven not by altruistic intentions of curbing black money and corruption, but for keeping up the faith of the masters, the MNCs and Big-Biz is all too evident now. With an estimated 150 lakh crore transactions between organizations and between individuals taking place annually, converting the economy to plastic and digital bits holds the prospects of enormous profits for MNCs as well as for the homegrown variety. No matter that the petty and small traders, who stood with the BJP all along, will be sacrificed at the altar of Big-Biz matters very little to the Modi brigade, as they owe their seat of power to Amabnis and Adanis. Keeping them in good humor is more important. That the dictates of neo-liberal order mandates that pliant regimes fall in line, no matter at how much the social and economic cost to the people has been witnessed in Mexico, Argentina, Bolivia and elsewhere. International financial oligarchy wants changes that can give free rein to their regimen, while killing local businesses. Anyway, the cards of nationalism and religious bigotry will come in handy when needed for BJP – they had used them successfully all along. But something had gone sour along the way to demonetization. By projecting himself as the face of this “heroic act”, he has also become the target of all those slogging in vain in serpentine queues for the last one month or so.

The RSS and its sister organizations had thrived all along by rumor mongering, whether to incite communal riots or to put Modi in power. The ‘jumla’ of depositing 15 lakh rupees in to every citizens’ account and the promise of jobs for youth had carried the day for BJP. Now, with distress in long queues before banks and ATMs morphing in to anger at the government, the Sangh outfits are busy again, with a whisper campaign that every Jan Dhan account holder is going to see 2 lakh rupees deposited in to their accounts anytime soon. Yes, people believe it, at least for now. A simple math tells us that with 26.8 crore or so Jan Dhan accounts opened in the country, the bounty to be dispensed by the Modi dispensation works out to 54 lakh crore rupees, amounting to about 3 yearly budgets. So far the governments have shown enthusiasm in showering the rich with tax incentives amounting about 6 lakh crore rupees in every successive budget. If the intention of forcing common citizens to deposit their money in banks with the excuse of demonetization, is intended to keep the banks afloat, then surely, dispensing the ethereal 54 lakh crore rupees will not only kill the banks along with the government – before we even ask where from that kind of money is going to come from. The Modi regime has to perform hara-kiri, if it wants to extract such a large amount of money from big businesses, who are the real fountainhead of black money. And there are more poor people in this country who do not possess a Jan Dhan account – depriving them of this ranbow bounty will surely make then sworn enemies of Modi. And what about the lower middle classes and the workers in the organized sector? How can the ruling party keep them from getting disgruntled for ignoring them?

When land was acquired from poor peasants in the name of development and they were paid small amounts, the money was mostly frittered away, rather than being put to productive use. What is sensible is that if this government, or for that matter any government wants development, they have to put the money at their disposal to productive use. Just 2 lakh crore rupees doled out by banks as loans, with some seed money given by government can gainfully provide livelihoods to 1 crore educated youth. They can be encouraged to set up mini food processing units, small solar power units, solar water purifiers, mini cold storage units etc., a measure which can go a long way in reviving our rural economy. And it is going to have a cascading effect in nurturing livelihoods and incomes for another 5 to 6 core youth in the form of jobs and secondary business opportunities. Which literally means that with just an expenditure of 2 lakh crore rupees every year, we can bring about 20 crore people out of the cycle of poverty and they will in turn expand the market by becoming consumers in their own right. This is what is really going to increase profits for businesses, by progressive expansion of the market, rather than by short cutting the banks with NPAs.

Vijaya Kumar Marla is a retired engineer and is presently the National Working President of All India Progressive Forum, an organization of progressive minded intellectuals, spread over 18 states in the country. ([email protected])