The abrupt demonetisation of 500 and 1000 rupee notes by the Narendra Modi regime is a drastic move that is staggering in its scale, ambition and repurcussions. The only other figures in modern history one can think of, devious or stupid enough to attempt something similar, are the likes of Marcos, Suharto, Idi Amin and Pol Pot.

For all its audacity however, the decision could go down also as the grandest of blunders made by anyone in Indian political history. Poorly planned and implemented it is likely to prove disastrous not only for the country’s economy but – ironically enough,– for the BJP’s own electoral fortunes.

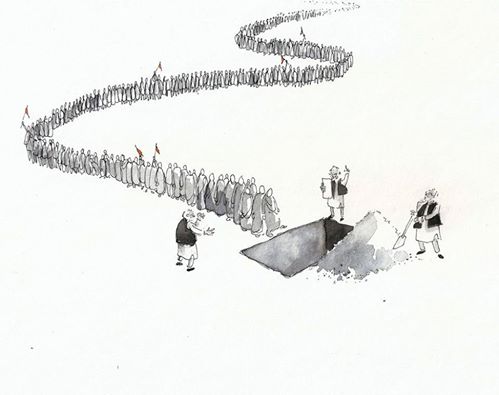

The abolition of the two currency notes – that make up 86% of all cash in circulation in the Indian economy – has affected almost every family in the second most populous nation on the planet. The harassment of the common citizen – particularly from the ranks of the urban and rural poor-through denial of access to income, savings and livelihood will not be forgotten anytime soon.

The Modi government’s supporters have termed demonetisation a ‘surgical strike’ against black money, calling it a ‘bold’ , ‘necessary’ and ‘well intentioned’ step. A more rabid section of his fans see all complaints as coming from those who benefited from black money, mainly the BJP’s political opponents. The Prime Minister himself has called upon the nation to ‘make sacrifices’ and put up with hardship for 50 days in this battle against corruption.

However, growing consensus among economists both within and outside the country is that demonetisation is a foolish measure and will hurt the Indian economy badly – especially farmers, small businesses, labour and anyone part of the country’s informal sector – and operates on a daily basis through cash transaction. The informal sector constitutes over 30 % of the Indian economy in value and 92% in terms of workforce employed[1].

Since the drastic policy was announced on November 8, all these have come to a complete standstill, leaving millions without livelihood or means to buy basic goods. As one respected economist has pointed out demonetisation may have permanently damaged India’s informal sector[2].

A severe deflation is predicted over the next six months to a year or even longer, as spending power disappears or goes down for millions of Indians and businesses shut down. There is also the concern that, with government issued currency losing credibility through demonetisation, more and more people will keep their money in unproductive but safe assets like gold and property.

So, why would the government take such a high risk step ? What was Mr Modi really trying to do when he announced a measure that directly affects almost every single family in the second most populous nation on the planet? Who are the real beneficiaries of this drastic policy? Will it really stop black money from circulating in the economy and end corruption from the country?

Despite all this propaganda it is quite clear now that demonetisation has nothing really to do with black money, that constitutes a sizeable 20 % of the Indian economy, of which only 6% is hoarded in cash, the rest being stashed away in gold, real estate and foreign accounts. If the government was serious about hurting the beneficiaries of black money they would have started by prosecuting those who keep such ill-gotten wealth in non-cash assets. Also, given the large-scale collusion of the Indian political class and bureaucracy in corruption the Modi regime should have first gone after its own ministers and government officials (particularly from the tax and revenue collection departments) to set a public example.

At its core, demonetisation is essentially an an attempt at economic and social engineering – on behalf of corporate banking and financial elites – the new paymasters Modi genuflects to after having ditched the small and medium mercantile lobbies the BJP represented for long. The Indian middle-classes, both real and aspirational, are rooting for the policy as they see a consolidation of their own power and future benefits in it.

With one stone, the policy’s architects have tried to slaughter many birds: recapitalise public banks burdened with bad loans; lend out new deposits to cronies in the corporate sector; enrich new entrants into the digital banking business, give the government extra funds to spend on its pet projects and steal a march over political rivals.

a. Rebooting troubled Indian banks: The bad loans or Non Performing Assets (NPAs) in the Indian banking sector, stood at nearly6 lakh crore rupees by end of March 2016[3]. Over 90 per cent of this is on the books of public-sector banks, with the State Bank of India accounting for the highest amount. Even this sum, stunning as it may be, is considered a gross underestimation and if loans that face the risk of being declared NPAs are also taken into account, theoverall stressed advances of Indian banks will double[4]. A bulk of the NPAs are in turn due to default on interest payments by the corporate sector, which has been milking the banking system through its political patrons.

The increase in deposits of banks expected due to the crackdown on black money is expected to help banks get into better health, lower interest rates and enable them to resume lending to Indian businesses again. In other words, demonetisation is a way of saving many Indian public sector banks while also providing corporates with fresh loans, a very dubious strategy given those in power seem to have no real will to recover money from their defaulter cronies.

b. Increasing the government’s cash flow: One of the justifications being given now for demonetisation is that an estimated Rs.16 lakh crores circulating in the Indian economy as cash, mostly in the form of 500 and 1000 rupee notes, will all get accounted for as they will be forced to go through the banking system. Assuming that a significant portion of the cash held in high denomination notes is ‘black money’ – it is argued that a significant percentage of this black money will not come back at all due to fear of penalties and prosecution and becomes useless. This will reduce the overall liability of the Researve Bank of India by anywhere between 2-4 lakh crore rupees, providing a windfall to the state exchequer. This calculation has been challenged by several economists but even if it were right, the moot question is what the government plans to spend all this extra money on, given its extremely poor record of spending on health, education and infrastructure for the welfare of the population?What is the guarantee that it will not all end up in the pockets of ruling party politicians and their businessmen friends?

c. Boosting the digital cash economy: In July this year a new study by Google and Boston Consulting Group[5] predicted an exponential increase in digital payments, estimated to grow by 10 times to touch US$500 billion by 2020 – or around 15% of the Indian GDP by that time. A bulk of these payments, the study said, will be micro-transactions, with over 50% of person-to-merchant business expected to be under100.

The biggest barrier to this prediction coming true however is supposed to be the fact that a vast majority of Indians prefer to use cash over digital money. Cash, as a percentage of total consumer payments in India, is around 98%, compared with 55% in the US and 48% in the UK, according to report by Payments Council of India released in 2015[6].

In one sweeping stroke, the Modi regime has changed all that and through demonetisation is about to force millions of Indians into the waiting arms of around a dozen private ‘payment banks’ given licences to operate by the Reserve Bank of India in 2015. Among the big non-banking sector corporate grabbing these licenses are Reliance Industries, Airtel, Aditya Birla group, Vodafone, Paytm and Tech Mahindra. The fact that Paytm[7] saw more than five-fold rise in overall traffic in less than 18 hours of the demonetization is an indication that ‘achche din’ have really arrived for the BJP’s cronies in the new banking sector.

Ironically (or maybe not so ironically) the total black money stored in digital form in foreign banks and in benami names in domestic banks and in shares, bonds and other financial instruments is much bigger than that in hard cash. In the absence of a honest political ruling class, bureaucracy or police the shift to a digital economy will only make it easier to store black money while making companies in the banking sector rich.

d. Cutting political opponents to size: Apart from all these dubious motives behind demonetisation there seems to be something even more devious at work. There are serious allegations of a scam–that BJP insiders changed their hoards of black money into white in various ways in the run up to the new policy. While these charges need further investigation, the Indian media has already reported a suspicious surge in bank deposits in the months just prior to demonetisaion and even produced evidence of the BJP’s West Bengal unit depositing large sums of cash[8] into its account just hours before the announcement was made. Given the widespread use of black money in cash by all political parties during elections demonetisation is calculated to hit the BJP’s opponents in the upcoming Punjab and Uttar Pradesh elections. Public discontent over the policy could however negate any such gains.

Looking at the demonetisation policy from a more long-term political perspective the portents under the current regime are scary. What Narendra Modi is really proving is that he is capable of playing a very high-risk game in order to boost his own stature, ram through policies that benefit his corporate cronies and care two hoots for the welfare of the Indian masses (despite being a chaiwallah’s son himself!). It is a display of high confidence, even arrogance, on part of the BJP ‘strongman’ that is extraordinary even by his previous record and standards.

The other point to note is that the Indian right wing, represented by the BJP and the Sangh Parivar, is not at all hesitatnt about turning the entire country or even the Indian Constitution upside down in pursuit of whatever objectives they deem worthwhile. In that sense the idea of ‘revolution’ or overthrow of the state and current social order, rhetorically championed for long by leftists, is being implemented in practice by the right-wing. The Sangh Parivar has become the only effective insurrectionary force in the country today- with truly frightening possibilities in future, including a political emergency to accompany the financial one.

This is not to say at all they will necessarily succeed in their plans. Fortunately for Indian democracy, those espousing fascist control also seem to be cocksure and foolish – as undoubtedly Modi and his men have been with the demonetisation decision –a truly spectacular self-goal on their part.

With public anger against the policy growing steadily this is perhaps the right time for opponents of the Parivar’s various, draconian gameplans to get their act together and mobilise the Indian people. How seriously they carry out this mission will determine whether it is the Parivar or its opponents who finally go out of circulation –like the recently abolished currencies.

Satya Sagar is a journalist and public health worker who can be reached [email protected]

[1]Indian Informal Sector: an Analysis Dr. Muna Kalyani. International Journal of Managerial Studies and Research (IJMSR) Volume 4, Issue 1, January 2016, PP 78-85. https://www.arcjournals.org/pdfs/ijmsr/v4-i1/9.pdf

[2] http://thewire.in/80564/modis-demonetisation-move-may-have-permanently-damaged-indias-informal-sector/

[3] http://economictimes.indiatimes.com/articleshow/51078318.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

[4] http://www.dnaindia.com/money/report-indian-banks-stressed-loans-pile-set-to-top-rs-13-lakh-crore-2211890

[5] http://www.livemint.com/Industry/M6SPyd4vUcC7QIQRnjBqaO/Digital-payments-in-India-seen-touching-500-billion-by-2020.html

[6] https://www.saddahaq.com/digital-india-epayments-and-online-transactions-upset-the-traditional-paper-payment-apple-cart-incentives-for-epayments-could-be-offered-in-the-budget

[7] http://www.livemint.com/Companies/iHcFkPVVuATAjxCD5zK4QJ/Digital-payment-platforms-record-surge-in-transactions-after.html

[8] http://economictimes.indiatimes.com/news/politics-and-nation/bengal-bjp-deposits-money-just-hours-before-currency-ban-announcement-cpm-alleges-tip-off/articleshow/55372157.cms